880

|

Believe it or not! Last night, in my dream, I—Panda3dp.com—joined forces with a consortium of investment institutions, banks, and listed companies to raise over 20 billion CNY (approximately 2.8 billion USD). With this immense capital, I swept up every publicly traded 3D printing company abroad, including Stratasys, 3D Systems, Nano Dimension, Materialise, Desktop Metal, Markforged, and Velo3D.

Subsequently, I systematically assimilated the technologies of these companies and relocated their production of printers, materials, and services to mainland China. By 2030:

1. Leveraging the abundant local engineering talent and the highly efficient supply chain, we slashed product and service costs by half and doubled operational efficiency. Overseas R&D and operational expenses had been draining net profits—costs that could be dramatically curtailed once moved to China.

2. Harnessing the massive dividends of China's manufacturing market, total revenue rose from $1.6 billion in 2024 to $4 billion by expanding 1.5 times.

3. Thanks to reduced costs, improved efficiency, and surging revenues, the combined net profit margin of our 3D printing tech group reached 20%, yielding $800 million in profits.

4. I then consolidated these assets into a single 3D printing holding conglomerate and listed it on the A-share market. The market responded with a price-to-sales ratio of 10, valuing the group at 290 billion CNY (around $40 billion USD). If valued at a PS ratio of 20, the valuation could even approach 600 billion CNY. As a pillar of additive manufacturing—alongside subtractive methods (like CNC machining) and formative techniques (like injection molding, forging, and casting)—3D printing truly earned its place in the future of global manufacturing.

5. In essence, through strategic acquisition and efficient operation, the 20 billion CNY we invested in 2025 transformed into 290 billion by 2030—a return of more than tenfold. We not only anchored the world’s leading 3D printing technologies in China, bolstering our manufacturing industry and even reshaping certain sectors, but also reaped substantial financial rewards. This is undeniably a vision worth pursuing!

However, when I woke up this morning, I found my pillow soaked and drool still lingering at the corner of my mouth—what a sweet, intoxicating dream of 3D printing glory!

What One Ponders by Day, One Dreams of by Night Though merely a dream, it was born from a day of deep contemplation.

Foreign 3D Printing Stocks Are Incredibly Cheap—China’s Valuations Are 20 Times Higher

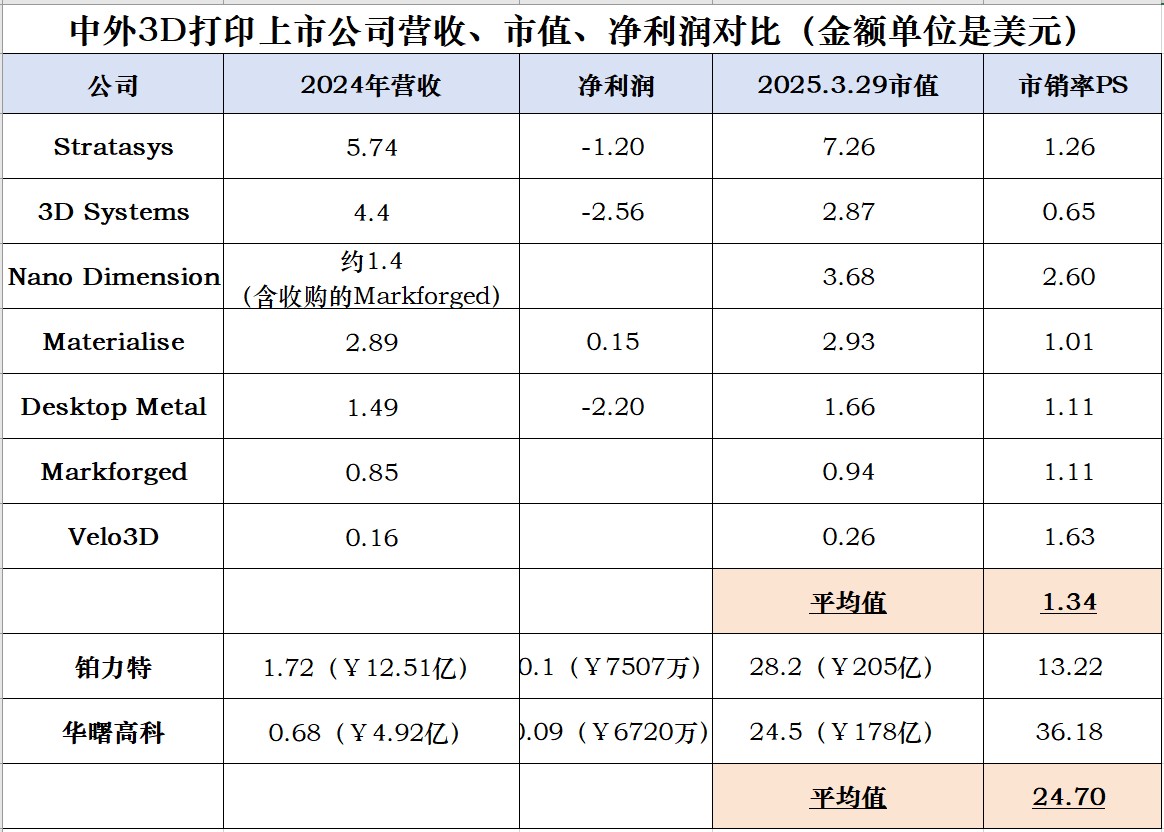

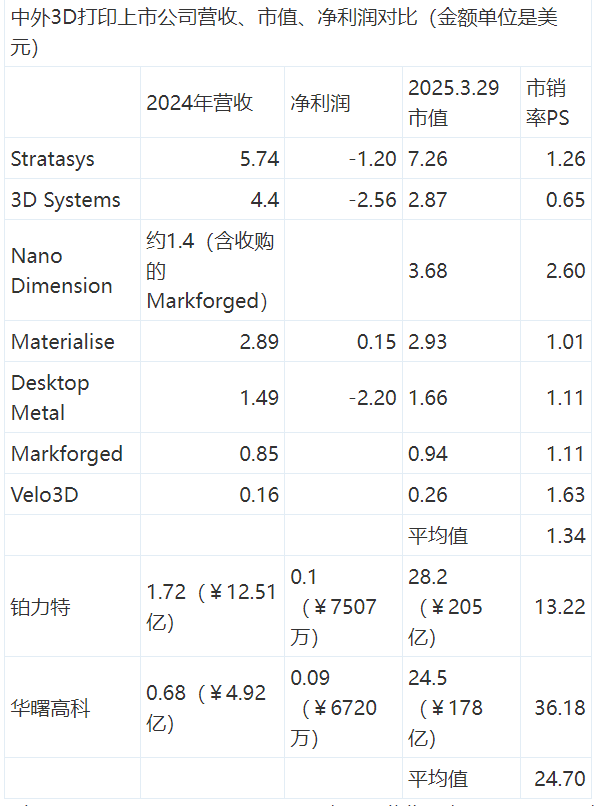

△Global 3D Printing Companies Ranked by Market Value – Chinese Firms Far Ahead (Data as of March 29, 2025)

To illustrate the financial feasibility of this 3D printing fantasy, I compiled the above chart comparing revenue, market capitalization, net profits, and price-to-sales ratios of Chinese and foreign publicly listed 3D printing firms. As most overseas companies are still operating at a loss, I opted for the PS ratio instead of the less suitable PE ratio.

△Chart: Panda3dp.com’s Comparison of Revenue, Market Value, Net Profit, and PS Ratio of Chinese and Foreign 3D Printing Companies

From the table, it is apparent that most U.S.-listed 3D printing companies have been suffering from perennial losses, with an average PS ratio of just 1.34. Meanwhile, the average PS ratio in China soars to 24.7. That means, if a 3D printing company generates annual revenue of 100 million CNY, it would be valued at 134 million on the U.S. market, but a staggering 2.47 billion on the Chinese market—a near 20-fold difference!

As the global epicenter of manufacturing, China holds tremendous promise for 3D printing applications—be it in aerospace, moldmaking, injection molding, healthcare, footwear, automotive, or, more recently, the booming metal 3D printing for mobile 3C devices. The large-scale deployment of 3D printing technology hinges on China, and market growth expectations are soaring. Thus, it makes sense that China’s capital markets assign significantly higher valuations to 3D printing companies than their Western counterparts.

Panda3dp.com strongly urges Chinese stakeholders to recognize that low-PS U.S. firms can become prime acquisition targets. China can gain cutting-edge technology and elevate its global standing through strategic buyouts.

The Technical Value of Acquiring Foreign 3D Printing Companies

Such acquisitions would grant China access to advanced overseas 3D printing technologies, along with complementary supply chains and market networks. Here's a breakdown of the technological highlights of these acquisition targets:

- Stratasys: Fused Deposition Modeling (FDM), PolyJet, Selective Absorption Fusion (SAF); focused on polymer printing and 3D printing software. - 3D Systems: Stereolithography (SLA), Selective Laser Sintering (SLS), Direct Metal Laser Sintering (DMLS); covers both polymers and metals, with software solutions. - Nano Dimension: Inkjet-based electronics 3D printing, specializing in circuit boards and other electronic components. - Materialise: Offers SLA, SLS, and Selective Laser Melting (SLM); mainly provides software and manufacturing services. - Desktop Metal: Binder jetting for metals/sand, DLP photopolymerization, and more. - Markforged: Continuous Fiber Reinforcement (CFR) for composites and Bound Powder Extrusion (BPE) for metal printing, plus software. - Velo3D: Laser Powder Bed Fusion (LPBF), with a focus on complex metal components.

Just Another Daydream? Could this grand vision merely be a flight of fancy?

From the perspectives of capital, market application, and valuation systems, such acquisitions are not out of reach. Panda3dp.com believes that with a mixture of cash and equity, China could offer a 20–40% premium over these companies’ current market caps and still close deals for 20 billion CNY. Most of them are already anxiously awaiting buyouts.

However, such acquisitions would inevitably be subject to scrutiny by the Committee on Foreign Investment in the United States (CFIUS). Nearly all these firms are involved in defense and military industries, some even holding substantial contracts and funding from the U.S. Department of Defense. Given today’s tense U.S.-China relations, there is a 99% likelihood such deals would be blocked.

In fact, Panda3dp.com previously assisted a domestic firm in bidding about 200 million CNY to acquire a European 3D printing company. But due to regulatory reviews from Europe and the U.S., legal counsel ultimately advised abandoning the acquisition. Cultural differences and integration challenges add further complexity.

Still, perhaps acquisition via entities based in Singapore or other jurisdictions might present a glimmer of hope. Interested institutions are welcome to add me on WeChat: lihaixiong. Let’s explore this dream together. |

The plan is to deploy 2,000 3D printers for footwear researc

Priced Around CNY200/kg, Withstands Over 190°C Without Cham

Meituan Enters the 3D Printing Arena — Leads Series B Inves

Grab It for Just CNY17,000 — Consumer-Grade Continuous Fibe

BLT’s Metal 3D-Printed Car Body Parts and Brake Calipers He

Apple Recruits a 3D Printing Expert in Shenzhen — Requires

Shenzhen Hymson, a Laser Tech Firm Valued at Over 10 Billion

5 μm Layer Thickness Achieved — Yunyao DeepVision Redefine

AM news | Email:bd@nanjixiong.com

China 3D printing | Record number | ©2024 panda3dp Team. Powered by panda3dp

Record number | ©2024 panda3dp Team. Powered by panda3dp

News

News