1645

|

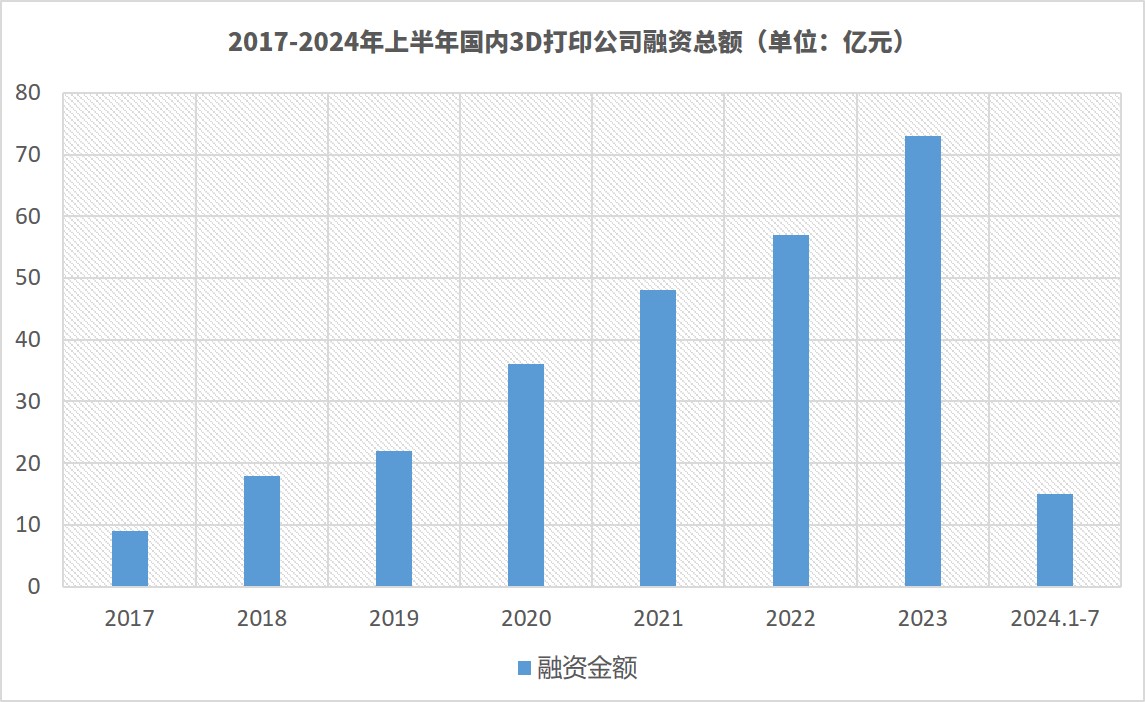

From 2017 onwards, Panda3dp.com has been closely monitoring the investment and financing activities of 3D printing startups in China. Over the past seven years, from 2017 to 2023, the 3D printing industry's investment and financing have consistently grown. Starting at 900 million CNY in 2017, it soared to 7.3 billion CNY in 2023, marking an eightfold increase. This growth reflects the expanding scale of the 3D printing industry and the increasing attention from the capital market. However, beginning in 2023, Panda3dp.com has sensed a downturn in the investment climate for the 3D printing sector, influenced by the broader economic environment. As Wusichun, the founder of Plum Ventures(梅花创投), mentioned in a talk show, "Nowadays, fundraising, investing, and entrepreneurship are all quite challenging."

Overview Throughout 2023, Panda3dp.com recorded 38 3D printing project financing cases in China, roughly on par with 2022. These 38 projects amassed a total financing amount exceeding 7.33 billion CNY, a 28% increase from the 5.74 billion CNY in 2022. Notably, two significant financing cases stand out: Bright Laser Technologies(铂力特) completed a private placement of over 3 billion CNY, and Farsoon High-Tech(华曙高科) successfully raised 1.105 billion CNY through an IPO on the STAR Market. These two financings alone accounted for 56% of the total industry financing. Excluding these two public companies, the remaining 3D printing companies secured 3.225 billion CNY in financing in 2023. Several leading projects, which had secured substantial financing in 2022, did not receive any or only minimal additional financing in 2023. In the first seven months of 2024, the investment and financing scenario for the 3D printing industry appeared bleak. Panda3dp.com recorded 11 financing cases with a total estimated amount of around 1.5 billion CNY, roughly 20% of the previous year's total, indicating a significant decline. Furthermore, no 3D printing company successfully went public in the first half of the year, although SCANTEC(思看科技), a 3D scanner manufacturer, is striving for an IPO on the STAR Market.

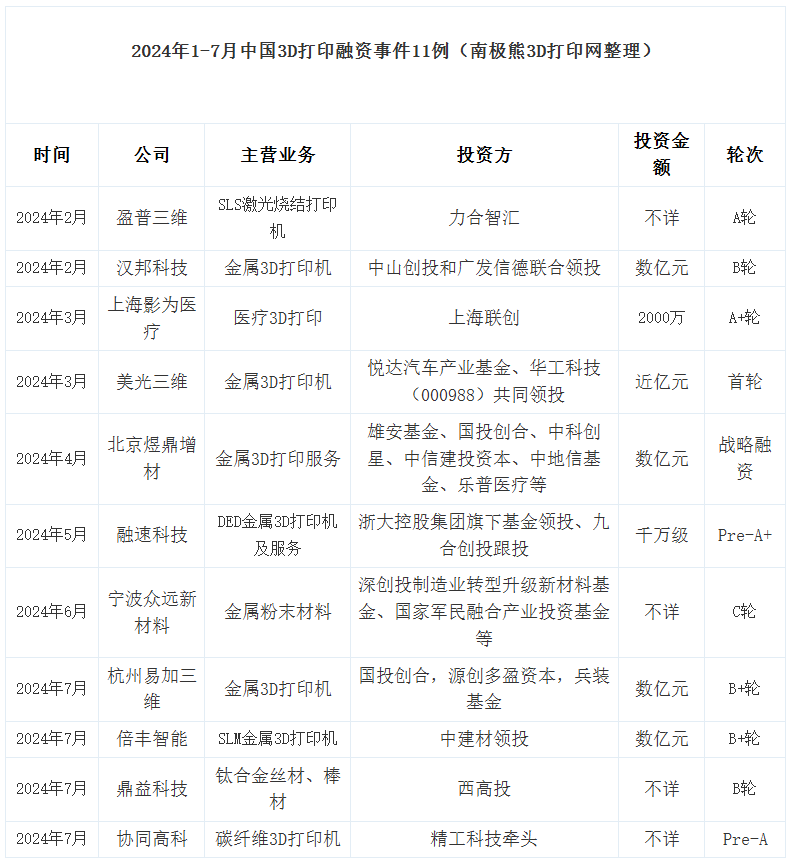

Analysis of Investment and Financing Cases In the first seven months of 2024, the 3D printing companies that secured investments include TPM3D(盈普三维), HBD(汉邦科技), Yingwei Medical(影为医疗), FastForm(美光三维), Yuding Additive(煜鼎增材), Rongsu Technology(融速科技), Zhongyuan New Materials(众远新材料), EPlus3D(易加三维), AmPro Innovations(倍丰智能), TIPRO GROUP(鼎益科技), and Xietong High-Tech(协同高科). According to Panda3dp.com, several 3D printing companies are in the process of completing financing exceeding 1 billion CNY, but these have not been finalized and are thus not included. These companies primarily focus on industrial 3D printers, materials, and application services, with a particular emphasis on metal 3D printing. Manufacturers of metal 3D printing equipment: HBD(汉邦科技), FastForm(美光三维), EPlus3D(易加三维), BLT(铂力特), and Rongsu Technology(融速科技). The first four are SLM metal 3D printer manufacturers, while Rongsu Technology(融速科技) specializes in DED metal equipment. Metal material suppliers: Zhongyuan New Materials(众远新材料) primarily offers metal powder materials, and TIPRO GROUP(鼎益科技) produces titanium alloy wires and rods. Non-metal 3D printing equipment manufacturers: TPM3D(盈普三维) is a veteran SLS selective laser sintering 3D printer manufacturer, and Xietong High-Tech(协同高科) produces 3D printing equipment for carbon fiber composite materials. Application service providers: Yuding Additive(煜鼎增材) offers metal 3D printing services for aerospace, and Yingwei Medical(影为医疗) provides 3D printing solutions for the medical field.

Summary Overall, the financing situation from January to July 2024 is not optimistic. Hopefully, more 3D printing enterprises will secure investments in the remaining five months of the year. Desktop 3D printer manufacturers, in terms of scale, are ready for an IPO, but with the tightening IPO environment in China, going public has become more challenging. Additionally, the market values of 3D printing companies in the secondary market have also experienced varying degrees of decline, as seen across the broader market. This can be referenced in the earlier report by panda3dp.com, "Market Values of 3D Printing Listed Companies Have Fallen Across the Board, Some Have Already Gone Bankrupt." This phenomenon has transmitted to the primary market, bringing a degree of uncertainty to startup financing. It is hoped that the 3D printing industry will achieve more breakthroughs in the second half of 2024, but companies must be prepared to face the harsh realities of the market. |

The plan is to deploy 2,000 3D printers for footwear researc

Priced Around CNY200/kg, Withstands Over 190°C Without Cham

Meituan Enters the 3D Printing Arena — Leads Series B Inves

Grab It for Just CNY17,000 — Consumer-Grade Continuous Fibe

BLT’s Metal 3D-Printed Car Body Parts and Brake Calipers He

Apple Recruits a 3D Printing Expert in Shenzhen — Requires

Shenzhen Hymson, a Laser Tech Firm Valued at Over 10 Billion

5 μm Layer Thickness Achieved — Yunyao DeepVision Redefine

AM news | Email:bd@nanjixiong.com

China 3D printing | Record number | ©2024 panda3dp Team. Powered by panda3dp

Record number | ©2024 panda3dp Team. Powered by panda3dp

News

News